.

How a Necessary Law Can Be Saved from Blocking Lobbyists

By Ann Rousseff

In December 2025, moderate Republicans in the House of Representatives and some Democrats filed filibuster petitions in Congress to force a vote on extending the Affordable Care Act (Obamacare) subsidies before they expire. These petitions are essentially formal attempts to bypass party leadership and bring the issue directly to the House of Representatives, or, for short, domestic politics.

On December 11, 2025, Representative Brian Fitzpatrick (R-PA) filed a filibuster petition to force a vote on a two-year extension of the Affordable Care Act (ACA) tax breaks. His proposal includes:

- Extending subsidies by two years.

- Adding income caps and minimum premium rules.

- Allowing enrollees to take a portion of the credit as a contribution to a Health Savings Account (HSA).

- Regulation of pharmaceutical benefits managers.

Representative Jared Golden (D-Maine) co-sponsored a similar bipartisan petition.

Another petition was filed by Representatives Josh Gottheimer (D-New Jersey) and Jen Keegan (R-Virginia) for a one-year extension.

What can we, the people who are not in the ruling party at either the state or federal level, do? We can:

Organize public petitions. Individuals and groups can start petitions through platforms like Change.org or MoveOn. While not legally binding, these petitions show public support and can put pressure on lawmakers.

OUR PETITION and link to it https://c.org/t4V5yf5qPp

Contact government officials directly. Calling, emailing, and writing to our members of the House and Senate is the most direct way to influence their actions. The offices carefully track voter sentiment, especially when thousands of people raise the same issue.

We Can Join Advocacy Groups: Organizations like Families USA, the National Health Council, and Protect Our Care are campaigning to extend ACA subsidies. Joining a group amplifies our voice through coordinated lobbying and media work.

State-level lobbying is also possible and can be paralleled by efforts directed at federal representative groups. Governors and state legislatures can create state-funded subsidies if federal ones expire. We Citizens can petition state officials to act at the local level, especially in states like Illinois, which may be more open to filling gaps.

Media and community action are another way to get your voice heard. Writing articles, attending town halls, and organizing public forums keep the issue visible. Local pressure often becomes national momentum.

A key difference between impeachment petitions and citizen petitions is that only legislators can submit and sign them, while public petitions, advocacy campaigns, and direct voter pressure are tools available to ordinary people. In short: while we as ordinary citizens cannot file formal impeachment petitions, we can create public petitions, organize campaigns, and put pressure on both federal and state officials. These local efforts often determine whether legislators are willing enough to compromise.

And here’s the background with some details:

The Affordable Care Act (Obamacare) is currently at a crossroads: its approved subsidies expire at the end of 2025, and Congress is deadlocked on whether to extend them. If no deal is reached, premiums could increase sharply in 2026, putting millions of Americans at risk of losing coverage. The approved subsidies (added during the Biden administration) that made ACA coverage more affordable for middle- and upper-middle-income households were in place. These subsidies are scheduled to expire on December 31, 2025.

Without renewal, premiums could increase by 20–30%.

For example, a household with an income of $85,000 could see annual premiums jump by $22,000 in 2026.

About 22 million Americans currently benefit from these subsidies, BUT:

Democrats want a “clean” extension of the subsidies for at least three years, and Republicans are divided, with moderates supporting extending the subsidies to avoid spikes in premiums for voters.

Conservatives oppose the extension, favoring alternatives like health savings accounts (HSAs), which would give individuals cash deposits but not reduce insurance premiums. They are slowly killing the law. The Senate, for its part, has blocked bills from both Democrats and Republicans, leaving the issue unresolved.

And access to health care is at stake. Studies show that losing full insurance coverage increases mortality. One study estimates that for every 52 people who get insurance, one life is saved.

As a result, families may be forced to choose between paying higher premiums, switching to cheaper plans, or dropping coverage altogether. Florida, for example, has 4.6 million residents under 65 who rely on ACA coverage.

Possible scenarios in this case are:

Subsidies extended. Then premiums remain capped at ~8.5% of income Coverage remains affordable for millions

Subsidies expire and premiums increase by 20–30% Millions could lose coverage or downgrade plans

HSAs replace subsidies, or rather, lump sum deposits for individuals. This means less coverage, higher deductibles, and certainly worse health outcomes.

The big picture today is that the ACA is more popular than ever in 15 years, but its affordability depends on whether Congress acts before the end of the year. If lawmakers fail to reach an agreement, 2026 could bring the biggest jump in health insurance costs since the law was passed. The trajectory of the ACA would then directly affect both consumer affordability and the broader insurance market.

Key impacts on seniors (50–64) in the event of a subsidy collapse will be that they will have no ACA benefits, and those with incomes just above 400% of the federal poverty level (e.g., $63,000 for a single person) will lose all assistance. And today’s $63,000 is yesterday’s $45,000. These are not living wages. Without subsidies, premiums could increase by 18–30% by 2026, doubling the cost for some seniors. And let’s not forget that the ACA allows insurers to charge seniors up to 3 times more than younger people. The loss of subsidies makes it impossible for these seniors to pay their premiums! 5.2 million of the population are in this group. And the knock-on effects on Medicare and Medicare Advantage will be sicker Medicare participants. When 50-64 year olds lose ACA coverage, they will delay their treatment until they become eligible for Medicare at age 65, and thus enter the program in poorer health, requiring more expensive interventions, namely untreated conditions leading to hospitalizations and chronic disease management. The end result will be a deterioration in Medicare and Medicare Advantage offerings.

And if, despite all efforts, the subsidies expire, we should expect a spike in plan premiums and a loss of coverage for millions of older adults and beyond. The ripple effect will also be felt in Medicare and Medicare Advantage, where risk pools will deteriorate as well as the quality of health of the people in them. Will Medicare’s financial health be in question?

The future of Obamacare directly shapes Medicare’s financial health. The decision to subsidize in 2025 is not just about the ACA, but about the sustainability of Medicare Advantage and supplemental health insurance over the next decade.

The chance that the ACA’s (Obamacare) individual insurance subsidies will be lost at the end of 2025 is very high. Both Democratic and Republican proposals to extend the subsidies failed in the Senate in December 2025. Neither party reached the 60 votes needed.

Republican leadership position: GOP leaders have signaled that they will not introduce an extension bill this year, and will instead push for alternatives such as health savings accounts.

Democratic position: Democrats continue to push for a clean three-year extension, but without bipartisan support, the measure cannot move forward.

What are the possible scenarios then? After all, this is not the first time the two parties have clashed over an important decision. And we know that in healthcare, the interests of both parties are concentrated.

The first scenario is a partial extension, which means that subsidies are renewed, but only for low-income households (e.g., below 400% of the federal poverty level). This will protect the poorest participants in the health insurance market. Middle-income families (such as those earning $60,000–$90,000) will lose support, facing increases in premiums.

The second scenario involves a short-term renewal in which Congress agrees to extend subsidies for 1-2 years while it negotiates a long-term solution. This buys political time, avoids an immediate premium shock in 2026, and the parties’ efforts are directed to other priorities. This would create uncertainty for insurers in setting prices, leading to cautious pricing (you know, lower prices).

There is also a Third Scenario where income-limited subsidies are offered, meaning subsidies continue but are phased out for those with higher incomes (e.g., households over $100,000). This would preserve affordability for most enrollees and reduce federal spending compared to a full extension.

There is even a Fourth Scenario which is a hybrid with an HSA. This would be a compromise where subsidies are cut, but policyholders would also receive deposits into health savings accounts. The impact of this option is to encourage consumer-driven care, but it does not reduce premiums. Even now, many subsidy recipients face affordability issues.

And Scenario Five involves state-level decisions

What this means: If Congress fails, states like California, New York, or Illinois could create state-funded subsidies to fill the gap. This option would create a large disparity in implementation between states and states with healthier and sicker populations.

The most likely outcome of the impasse would be a short-term renewal or partial extension in 2026, as both parties want to avoid the political fallout from losing millions in coverage. We gained time to act ! Wow!

Spread the petition: https://c.org/t4V5yf5qPp

The least likely outcome is a full permanent extension, given budget concerns and partisan divisions.

The most likely window for compromise is in the spring-summer of 2026, during budget negotiations and filings with insurers.

The political tipping point is the midterm elections in the fall of 2026; the subsidy expiration is a major campaign issue.

The impact on Medicare will be felt until June 2026. Then the MA (Medicare Advantage) offers will already reflect higher-risk groups if the subsidies remain expired, which will ensure the effects for 2027.

The president advocates for the option that, according to him, can have the greatest share in suppressing rising health care prices, but it is unlikely that the creation of an HSA will be a factor and a sufficient tool in the hands of the insured to influence these large insurance companies that dictate the market. The Republicans, including him, conveniently forgot how they invalidated the law by eliminating mandatory health insurance for citizens. Only with it could the insured have the power to influence insurers and assert their right to an affordable price. Now they can simply tell him: well, it is not mandatory to get insurance, right?! And all actions that arise from such a starting point are at least cynical. They are a violation of the human right to live with dignity by receiving treatment when necessary. From a purely technical point of view, insurance requires as large a group of insured persons as possible and the potential participation in this group to be more predictable, in order to have lower and more stable prices.

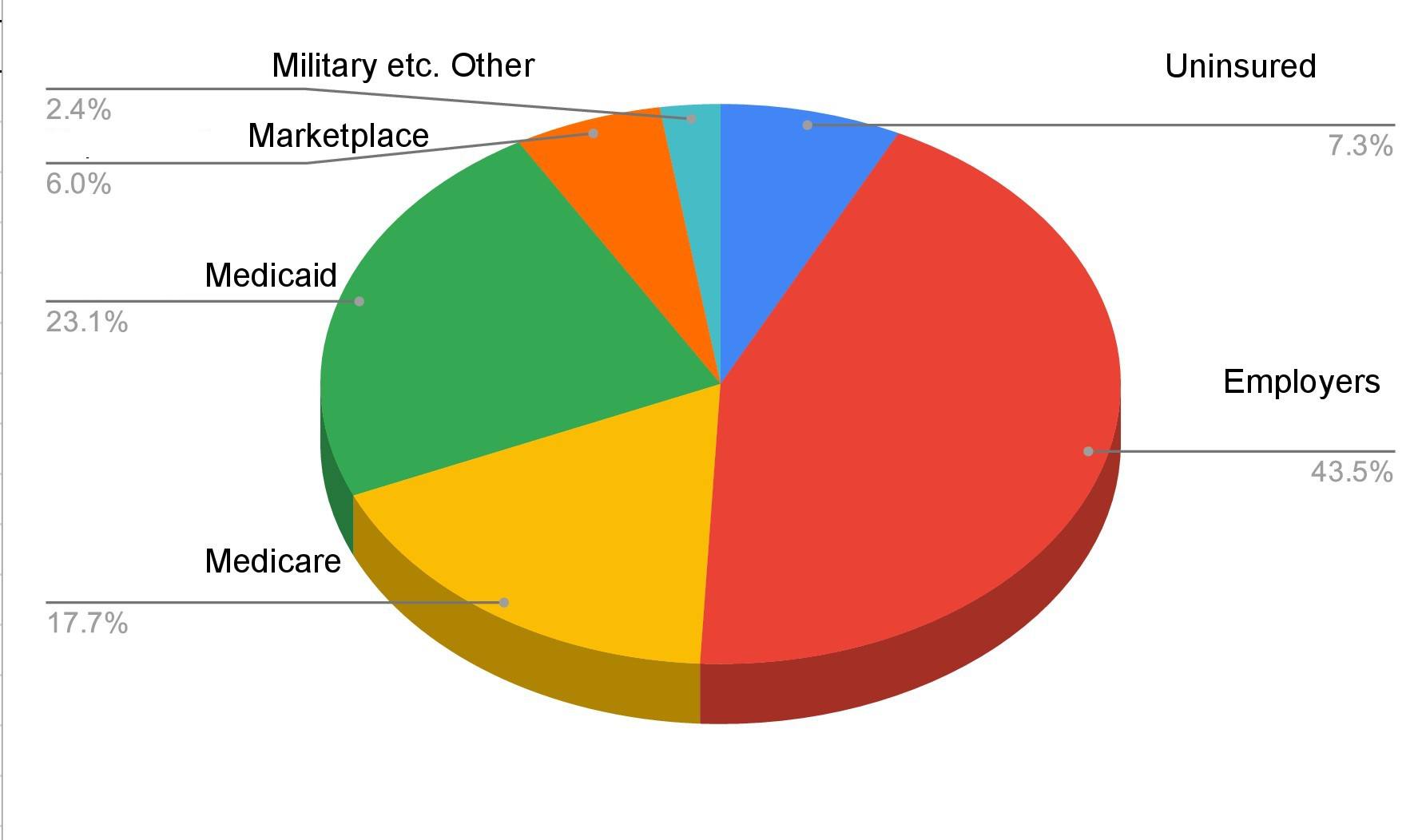

Now, about 27 million citizens remain uninsured.

Children (ages 0–17):

About 3.7 million children are uninsured.

That’s about 5.1% of all children.

Reason: gaps in Medicaid/CHIP enrollment and administrative barriers.

Working-age adults (ages 18–64):

The largest group of uninsured – about 11.6% of all people in that age group.

That’s over 22 million people.

People in states without Medicaid expansion are particularly affected (17.4% uninsured vs. 9.3% in states with expansion).

Adults over 65:

Almost all have Medicare coverage.

The uninsured are less than 1%, mostly people without enough work credits for Medicare and without access to private insurance.

.

History is spinning and accelerating backwards. 2025 will be the last year with such a high level of voluntary insurance of 22 million. It is sad for a country like a The USA to abandon its citizens without guaranteed health insurance. Domestic plunder is reaching a new peak here too.

Based on materials from the press WBUR, CDC/NCHS (National Center for Health Statistics), ACS (American Community Survey), Timeline of 2026 ACA Subsidy Decisions and others and my opinions. [email protected]

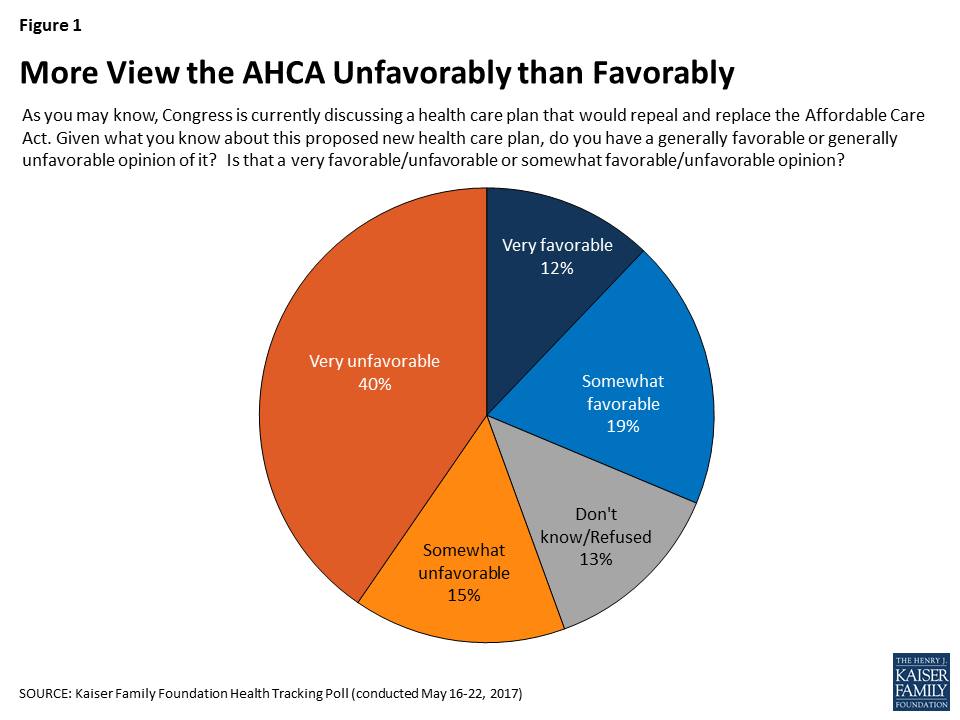

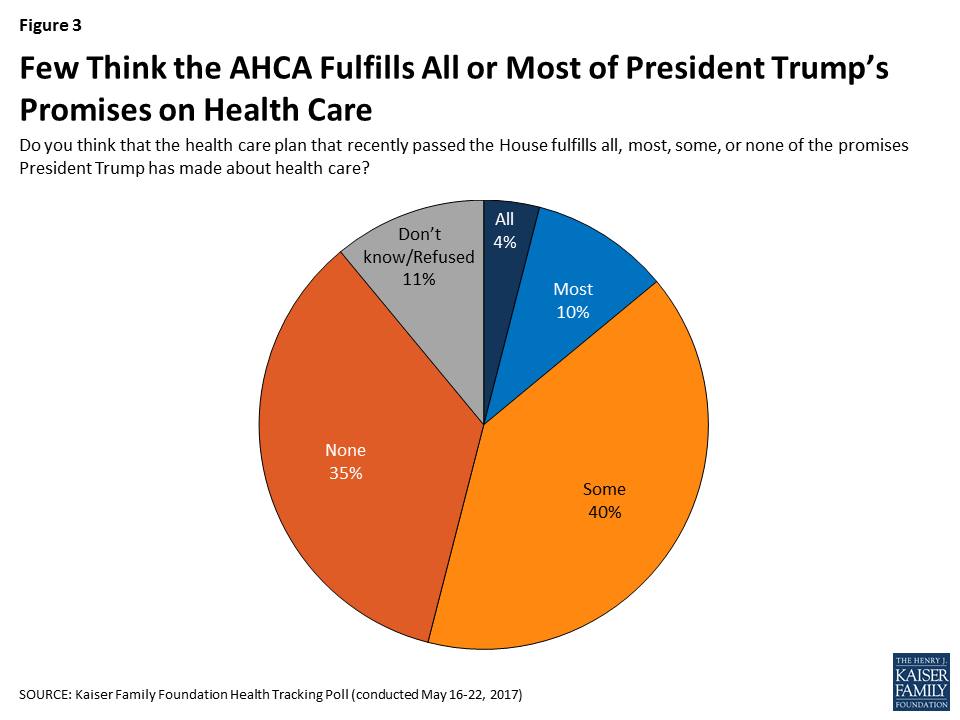

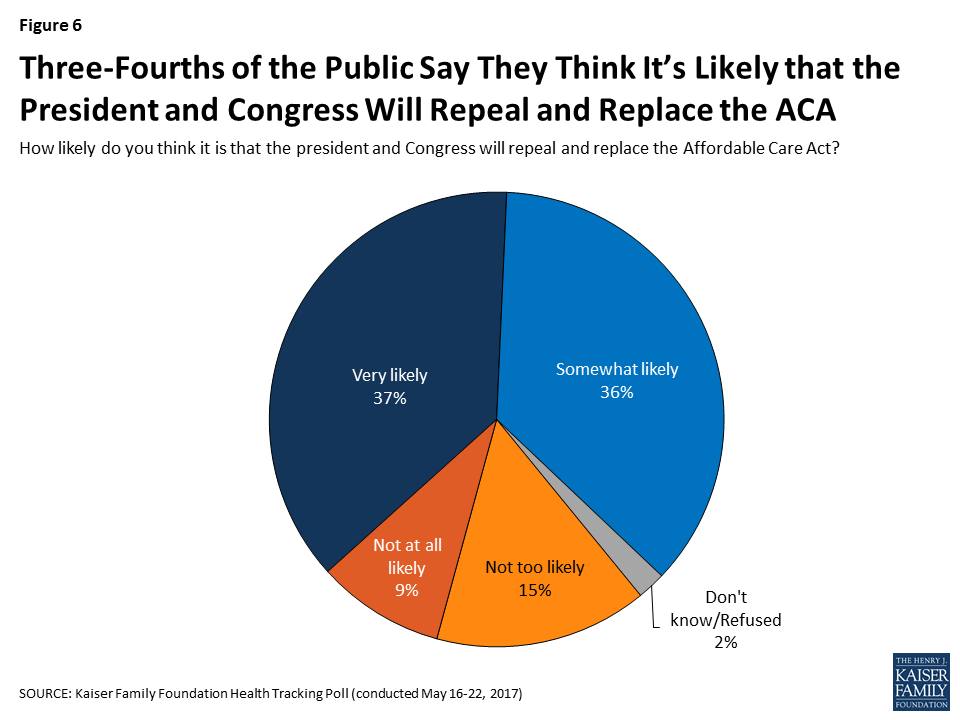

And more information regarding the attitude towards the modification proposed by the Republicans:

.

.

.